摘要

2008 年底,党中央、国务院为进一步扩大当前的市场内需,实现经济的稳定发展,以此为引导,和相关部门经过商讨之后,制定了相关的十项措施,最重要的一项措施就是,尽快实现保障性安居工程的建设与开发,尽快投入使用。这是一次重大的改革和创新,是一次大胆的尝试和实践,具有重要的实践意义和研究价值。

党的十九大再次作出“房子只能用来居住,不能用于其他非法行为或活动,严禁炒房等行为出现,应重视大众的住房供需平衡,实施多角度的保障措施,对当前的住房制度进行完善和升级,真正实现所有人民住有所居的目标和任务”。

近年来,在相关参与主体的不懈努力和共同付出下,我国保障性安居工程建设事业成绩喜人,形势一片大好。不过需要注意的是,这个过程中或多或少地暴露了一些问题,亟需得到相关部门的重视和关注,分析查找出现这些问题的原因,尽快进行完善和整改。一言以蔽之,保障性安居工程建设工作的开展时间紧,任务重。

在当前背景下,应关注保障性安居工程绩效的审计开展,建立完善的监督机制,确保保障性安居工程政策可以得到有效的落实,实现住房保障法规制度的快速发展和健全。同时提升保障性安居工程的质量和效率,保障参与主体的合法权益不受外界的影响和干扰,这才是当前时代环境中我国审计领域需要处理和解决的重点难题。

本文通过文献研究、案例分析和问卷调查等方法,对保障性安居工程的绩效审计进行研究和分析。研究内容大致可分为理论研究和案例研究两个部分。

前三章为理论研究部分,首先介绍了本文的研究背景和研究的目的,总结整理了国内外相关的研究现状。然后,以保障性安居工程绩效审计的相关概念为切入点,从公共受托经济责任理论、新公共管理理论和平衡记分卡理论来构建本文的理论框架,为本文的研究提供理论基础。其次,分别从审计内容的设计、审计目标的制定和审计方法的应用等维度出发,实现了保障性安居工程绩效审计相关理论结构的构造,最后通过阅读文献、整理资料和询问专家等,借鉴实际审计中运用的评价指标,将平衡记分卡的原理与绩效审计相结合,构建保障性安居工程绩效审计评价指标体系。第四章进行案例分析。运用第三章构建的评价指标体系,并采用层次分析法对指标权重进行赋值,对 A 市 B 区保障性安居工程绩效审计进行评价,并对审计结果进行分析。第五章总结全文,并针对问题提出完善对策建议。

本文尝试将平衡记分卡应用于保障性安居工程的绩效审计评价指标的构建之中。根据保障性安居工程项目的具体特点,对平衡记分卡的基本模型进行了适当的修正。将平衡记分卡原有的四个维度修正为效益维度、公众维度、内部流程维度和可持续发展维度。采用修正后的平衡记分卡对 A 市保障性安居工程项目进行绩效审计,是本文的研究创新之处。

关键词:保障性安居工程;绩效审计;平衡记分卡

Abstract

Atthe end of2008,in order to further expandthe current domestic market demandand achieve stable economic development, the Party Central Committee and the StateCouncil, guided by this, andafter discussion with relevant departments, formulated tenrelevant measures. The most important one is to realize the construction anddevelopment of indemnificatory housing project as soon as possible and put it into useas soon as possible. This is a major reform and innovation, a bold attempt andpractice,with important practical significance and research value.

Atthe 19th National Congress of theCommunist Party ofChina, it wasonceagainmade that "housescan onlybeused for living, not for other illegal activities oractivities,and it is strictly prohibited to fry houses. We should pay attention to the balance ofhousing supply and demand of the public, implement multi angle security measures,improve and upgrade the current housing system, and truly achieve the goal and taskof all people living in a certain place". In recent years, with the unremitting efforts andjoint efforts of relevant participants, the construction of indemnificatory housingproject in China has achieved gratifying results, and the situation is very good.

However, it should be noted that some problems are more or less exposed in thisprocess, which need to be paid attention to and concerned by relevant departments,analyze and find out the causes of these problems, and improve and rectify as soon aspossible. In a word, the construction of indemnificatory housing project has a shorttime and a heavy task.

In the current context, we should pay attention to the audit of the performance ofindemnificatory housing project, establish a perfect supervision mechanism, ensurethat the policy of indemnificatory housing project can be effectively implemented, andrealize the rapid development and improvement of housing security laws andregulations. At the same time, to improve the quality and efficiency of theindemnificatory housing project, and to ensure that the legitimate rights and interestsof the participants are not affected and interfered by the outside world, are the key problems to be solved in the audit field in the current era.

Through literature research, case analysis and questionnaire survey, this paperstudies and analyzes the performance audit of indemnificatory housing project. Theresearch content can be roughly divided into two parts: theoretical research and casestudy.

The first three chapters are the theoretical part. Firstly, it introduces the researchbackground and purpose of this paper, and summarizes the related research status athome and abroad. Then, taking the related concepts of performance audit ofindemnificatory housing project as the starting point, the theoretical framework of thispaper is constructed from the theory of public entrusted economic responsibility, thenew public management theory andthe Balanced Scorecard theory, which provides thetheoretical basis for the research of this paper. Secondly, from the design of auditcontent, the formulation of audit objectives and the application of audit methods, wehave realized the construction of the theoretical structure of the performance audit ofindemnificatory housing project. Finally, by reading the literature, sorting out thematerials and asking the experts, we use the evaluation indicators used in the actualaudit for reference, and combine the principle of the Balanced Scorecard with theperformance audit to build the guarantee Performance audit evaluation index system ofsex housing project. The fourth chapter carries on the case analysis. Using theevaluation index system constructed in the third chapter, and using the analytichierarchy process toassign theindex weight, this paper evaluates the performance auditof indemnificatory housing project in B District ofa city, and analyzes the audit results.

The fifth chapter summarizes the whole paper, and puts forward some suggestions tosolve the problems.

This paper attempts to apply the Balanced Scorecard to the construction ofperformance audit evaluation indicators ofindemnificatory housing project. Accordingto the specific characteristics of indemnificatory housing project, the basic model ofbalanced scorecard is modified appropriately. Theoriginal four dimensions ofbalancedscorecard are revised to benefit dimension, public dimension, internal process dimension and sustainable development dimension. Using the revised balancedscorecard to audit the performance of a city's affordable housing project is theinnovation of this paper.

Key Words: Affordable Housing Projects; Performance Audit; Balanced Score Card.

目 录

第一章 绪论·······················································································1

第一节 研究背景及意义························································································1

一、研究背景 ··········································································································1

二、研究意义 ··········································································································2

第二节 文献综述····································································································3

一、保障性安居工程研究·························································································3

二、绩效审计研究 ···································································································6

三、保障性安居工程绩效审计研究···········································································8

四、文献述评 ········································································································10

第三节 研究内容及方法······················································································11

一、研究内容 ········································································································11

二、研究方法 ········································································································11

三、技术路线 ········································································································12

第四节 创新点······································································································13

第二章 相关概念和理论基础···························································14

第一节 相关概念··································································································14

一、保障性安居工程的概念 ···················································································14

二、保障性安居工程绩效的概念············································································14

三、保障性安居工程绩效审计的概念 ·····································································15

第二节 理论基础··································································································15

一、公共受托经济责任理论 ···················································································15

二、新公共管理理论······························································································16

三、平衡记分卡理论······························································································17

第三章 基于平衡记分卡的保障性安居工程绩效审计体系构建······19

第一节 保障性安居工程绩效审计的目标··························································19

一、总体目标 ········································································································19

二、具体目标 ········································································································19

第二节 保障性安居工程绩效审计的内容··························································20

一、安居工程目标任务的落实和政策的贯彻力度····················································20

二、安居工程资金筹集、管理以及相应的使用情况················································21

三、安居工程住房建设和管理效果·········································································21

四、以前年度问题整改情况 ···················································································22

第三节 保障性安居工程绩效审计步骤······························································22

一、保障性安居工程总体情况················································································22

二、项目资金筹集、管理和使用情况 ·····································································23

三、安居工程住房建设进度和使用情况··································································23

四、以前年度问题整改情况 ···················································································24

第四节 基于平衡记分卡的保障性安居工程绩效审计评价指标体系··············25

一、平衡记分卡模型的修正 ···················································································25

二、保障性安居工程绩效审计的评价指标制定和分析·············································25

三、评价指标的权重赋值·······················································································29

四、综合评价 ········································································································30

第四章 案例分析·············································································32

第一节 我国保障性安居工程绩效审计现状······················································32

一、保障性安居工程审计基本情况·········································································32

二、保障性安居工程绩效审计存在的问题······························································34

第二节 A 市 B 区保障性安居工程绩效审计介绍···············································35

一、基本情况 ········································································································35

二、绩效审计目标 ·································································································36

三、绩效审计的内容······························································································37

四、绩效审计步骤 ·································································································37

第二节 A 市 B 区保障性安居工程绩效审计评价指标·······································39

一、绩效审计评价指标 ··························································································39

二、确定指标权重 ·································································································40

三、绩效审计综合评价 ··························································································45

第三节 A 市 B 区保障性安居工程绩效审计结果与分析···································50

一、绩效审计结果 ·································································································50

二、绩效审计结果分析 ··························································································53

第五章 相关建议与结论··································································55

第一节 完善保障性安居工程绩效审计的建议··················································55

一、完善相关的绩效审计评价指标体系··································································55

二、健全和完善相关法律法规体系·········································································55

三、建立与审计结果相挂钩的奖惩机制··································································55

第二节 结论··········································································································56

参考文献··························································································58

附录 A·······························································································62

附录 B·······························································································66

致谢··································································································67

第一章 绪论

第一节 研究背景及意义

一、研究背景

2008 年底,党中央、国务院为进一步扩大当前的市场内需,实现经济的稳定发展,以此为引导,和相关部门经过商讨之后,制定了相关的十项措施,最重要的一项措施就是,尽快实现保障性安居工程的建设与开发,尽快投入使用。这是一次重大的改革和创新,是一次大胆的尝试和实践,具有重要的实践意义和研究价值。

多年来,在相关参与主体的共同努力和相互配合下,全国保障性安居工程的建设和发展获得了一定的进展,效果显着,成绩喜人。一是完善了当前存在的住房保障体系。二是建设力度持续加大。三是政府投入大幅增加。四是经验逐步积累,认识不断提高。五是广大群众得到了实惠。同时也出现了一些矛盾和问题,亟需解决。假设不能有效的对这些问题进行处理,那么可能会对保障性安居工程建设和开发产生消极的负面影响,不利于效益性、效率性的体现,导致后续完成的程度和预期之间存在较大的差距,总之,保障性安居工程的时间紧,任务重。

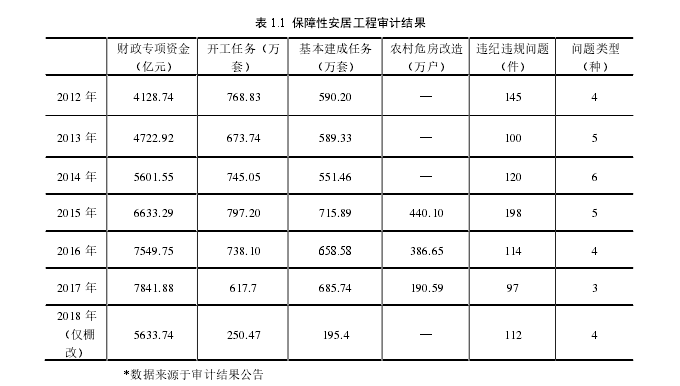

从 2012 年之后开始一直到现在,国家审计署的相关部门以及地方的审计机关都对保障性安居工程的实施效果较为关注,在全国范围内着力于保障性安居工程相关政策的落实与贯彻,由此可见,国家政府和相关审计部门对保障性安居工程的应用和实践效果非常重视。在“十三五”相关会议上,国家审计署结合当前经济发展形势和市场经济发展进度,明确了国家审计工作未来的前进方向,详细解读了城镇化建设的重要性,并多次强调,保障性安居工程相关工作务必尽快提上日程,不可延误,否则将失去先机,处处掣肘。对 2012 年到 2019 年期间的全国保障性安居工程审计结果进行整理和总结,详细内容可参考表 1.1。

目前,我国保障性安居工程审计的重点是在真实性、合法性上,相应的绩效审计力度较弱,也没有科学合理的评价机制。在此基础上,需要针对保障性安居工程绩效审计的相关工作,制定科学合理的监督管理机制,对保障性安居工程的相关制度进行完善和健全,及时关注政策落实的情况好效果,明确相关部门的详细职能和义务,严格遵循相关原则和规范开展实践的工作,定期向上级汇报工作进度,及时发展工作开展过程中出现的各项问题。

二、研究意义

现如今,社会经济持续快速发展,推动了城镇化建设发展的进程,保障性安居工程成为了一项重要的民生工程,是当下的热点问题。对保障性安居工程绩效审计进行研究,具有重要的理论和实践意义。

(一)理论方面

保障性安居工程绩效审计在我国是近几年才开始开展的,因此对该领域的相关研究并不多,缺乏丰富的参考依据。在本文的相关研究过程中,对保障性安居工程绩效审计相关的研究进行了整理和总结,涉及了多个维度的文献研究。本文根据平衡记分卡(简称 BSC)的基本原理,结合 A 市 B 区保障性安居工程绩效审计的实际案例,从效益、公众、内部流程和可持续发展四个维度出发,对保障性安居工程绩效审计目标进行细化,结合实际需求选择合理的维度,制定科学的绩效审计评价指标,经过实践验证,逐步形成较为完善健全的绩效审计体系,对保障性安居工程相关的绩效审计工作进行深入的研究和探索,尽快建设和我国国情相符合的保障性安居工程绩效审计的理论框架,具有一定的理论意义。

(二)实践方面

保障性安居工程作为一项直接关系人民群众切身利益的民生工程,对其开展绩效审计,可以切实维护好人民群众的利益不受侵害,有助于促进我国社会稳定以及全面小康社会的建设。本文在已有的理论基础上,结合实际案例,为今后审计机关开展此类业务提供参考和依据,具有实践指导意义。

…………由于本文篇幅较长,部分内容省略,详细全文见文末附件

第四章 案例分析

第一节 我国保障性安居工程绩效审计现状

一、保障性安居工程审计基本情况

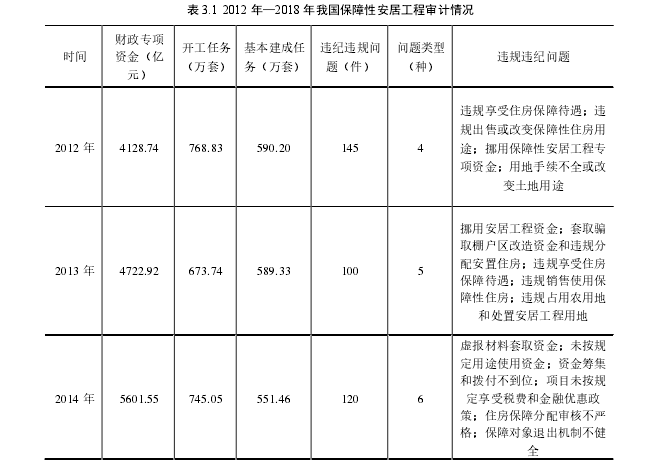

参考 2012 年至 2018 年之间的数据和研究结论发现,对于单个年限来说,审计署往往会组织各级审计机关进行讨论和研究,对国内大部分省份和自治区、直辖市的保障性安居工程资源投入情况进行总结和整理,借助相关的审计指标和体系开展相关的审计工作,对安居工程获取的成效进行评估和分析,从而发现在整个阶段内出现的问题,并提出科学有效的对策和处理方案,吸取教训,发扬优点,实现优化与升级,审计情况如表 3.1 所示。

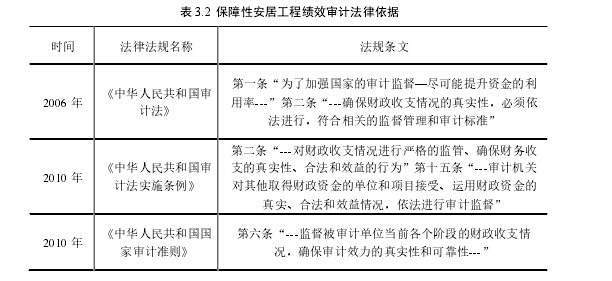

在保障性安居工程相关绩效审计工作的开展过程中,一般涉及诸多法律法规和政策意见,详情可参考依据的法律法规和政策文件见表 3.2。

二、保障性安居工程绩效审计存在的问题

(一)缺乏统一的绩效审计评价指标体系绩效审计指标在绩效审计工作的开展过程中,扮演了重要的角色,是不可或缺的关键因素,一般将其作为评估分析被审计单位或项目绩效实施力度的参照,借助该指标的应用,可以实现对保障性安居工程的客观、准确评价,能够帮助我们对工程实施过程中出现的诸多问题和缺陷进行直观的了解,对于绩效审计目标和任务的完成具有重要的作用。一直以来,国内住房项目审计都会涵盖诸多领域和层面,使得审计标准的设计和制定存在一定的难度,通常会出现指标体系不完善等问题,评价标准不确定,评价方法难以统一,无法完善科学健全的绩效评价指标体系,对保障性安居工程绩效审计工作的开展产生一定的负面影响。

(二)绩效审计法律法规相对缺失

就当前而言,保障性安居工程审计主要依据《中华人民共和国审计法》、《中华人民共和国国家审计准则》和审计机关发布的审计工作方案。需要注意的是,在实际的应用和实践过程中,由于相关的法律法规中暂未针对审计方案的实施进行明确的规定,缺乏绩效审计相关的规范制度,也没有针对绩效审计设置具体评价标准和评价指标,使得审计工作缺失专业的判断参考,影响审计的效率和质量。应尽快健全和完善科学合理的审计准则,否则将会导致绩效审计工作出现可操作性差的相关问题,对保障性安居工程的绩效审计发展极为不利,不利于长期的稳定发展。对于不同区域和地方来说,即使是同一审计事项,也会在内容、形式以及评估标准上存在不一致,也影响了保障性安居工程审计的整体质量和工作成效。

(三)屡审屡犯问题严重

在实际的操作过程中,应明确审计署的职能和责任,确保审计署的组织和领导功能得以最大化的实现,通过严格的监督和管理,在各级审计机关的共同努力下,发现了数量较多的违规违纪活动,相应的审计效果较为明显。不过对近七年来的审计结果进行分析和研究发现,常见的问题基本只有几种类型,但是就是这些简单的问题,居然每年都会重复出现,简单来说,就是地方相关部门明知道问题出在哪里,但是在下一年又会犯同样的错误,导致屡审屡犯的情况严重,这种情况务必得到彻底的处理,否则将会对我国审计工作的发展和进步造成严重的影响。目前,审计机关可以将审计中发现的挪用资金、住房诈骗等重大违法违纪问题,直接移送检察机关依法查处。但是,针对个别程度较浅的问题,仅实施及时整改或是提醒整改的相关处理方案,不重视整改的效果和效率,从长远来看,审计结果和审计建议将失去其重要性。

参考文献

[1] 蔡春,刘学华等.绩效审计论[M].北京:中国时代经济出版社,2006.

[2] 陈晖.廉租房项目绩效审计的内容和方法研究[J].广西财经学院学报,2012,25(04):104-107.

[3] 陈语斯. Y 市政策落实情况跟踪审计研究[D].南华大学,2019.

[4] 邓中美.保障性住房的社会评价[J].中国住宅设施,2008(06):16-17.

[5] 扶思妍.保障性安居工程绩效审计研究[D].云南财经大学,2018.

[6] 傅金龙.层次分析法在综合评分中的应用[J].农业技术经济,1987(05):6-8.

[7] 顾维萌.我国保障性住房政策绩效审计评价体系研究[J].当代经济,2017(13):100-101.

[8] 韩书英.大数据技术在保障性安居工程审计中的探索与应用[J].时代金融,2019(18):60-61.

[9] 何勇,江涛.保障性安居工程审计应着力”四个关注”[J].审计月刊,2014(12):45.

[10] 何元斌,王雪青.保障性住房建设中中央政府与地方政府的博弈行为分析[J].经济问题探索,2016(11):39-44.

[11] 洪伶.A 市保障性安居工程绩效审计案例研究[D].湘潭大学,2017.

[12] 黄梦媛.我国保障性住房绩效审计探讨[D].江西财经大学,2018.

[13] 姬艳红,王大帅.保障性安居工程审计探析[J].中国内部审计,2018(08):78-81.

[14] 蒋超博,朱立辉.城镇保障性安居工程资金绩效审计目标和内容[J].审计研究,2014(04):14-18.

[15] 李克强.大规模实施保障性安居工程 逐步完善住房政策和供应体系[J].求是,2011(08):3-8.

[16] 李静.保障性住房资金绩效审计研究——以某市为例[J].财政研究,2014(11):23-27.

[17] 李若愚.加快构建和完善我国住房政策性金融体系[J].宏观经济管理,2015(06):39-41.

[18] 李素利.政府绩效审计发展的影响因素研究[J].审计研究,2013(02):27-33.

[19] 李岩松.基于平衡计分卡的高校绩效审计评价体系研究[J].财经界(学术版),2016(22):284.

[20] 李玲.保障性住房项目的质量管理体系研究[D].武汉理工大学,2011.

[21] 李凌霄.保障性安居工程跟踪审计研究[D].浙江工商大学,2019.

[22] 刘煦.慈善基金绩效审计指标体系设[J].江苏商论,2014(08):85-88.

[23] 刘洛欣. Y 县保障性安居工程跟踪审计的案例分析[D].江西财经大学,2018.

[24] 刘音延.”三公”经费绩效审计评价指标体系研究及案例分析[D].西南交通大学,2017.